Compute Generalized or Orthogonalized Impulse Response Functions (IRFs) from

mvgam models with Vector Autoregressive dynamics

Usage

irf(object, ...)

# S3 method for mvgam

irf(object, h = 10, cumulative = FALSE, orthogonal = FALSE, ...)Arguments

- object

listobject of classmvgamresulting from a call tomvgam()that used a Vector Autoregressive latent process model (either asVAR(cor = FALSE)orVAR(cor = TRUE); seeVAR()for details)- ...

ignored

- h

Positive

integerspecifying the forecast horizon over which to calculate the IRF- cumulative

Logicalflag indicating whether the IRF should be cumulative- orthogonal

Logicalflag indicating whether orthogonalized IRFs should be calculated. Note that the order of the variables matters when calculating these

Value

An object of mvgam_irf-class containing the posterior IRFs. This

object can be used with the supplied S3 functions plot.mvgam_irf()

Details

See mvgam_irf-class for a full description of the quantities that are

computed and returned by this function, along with key references.

Examples

# \dontrun{

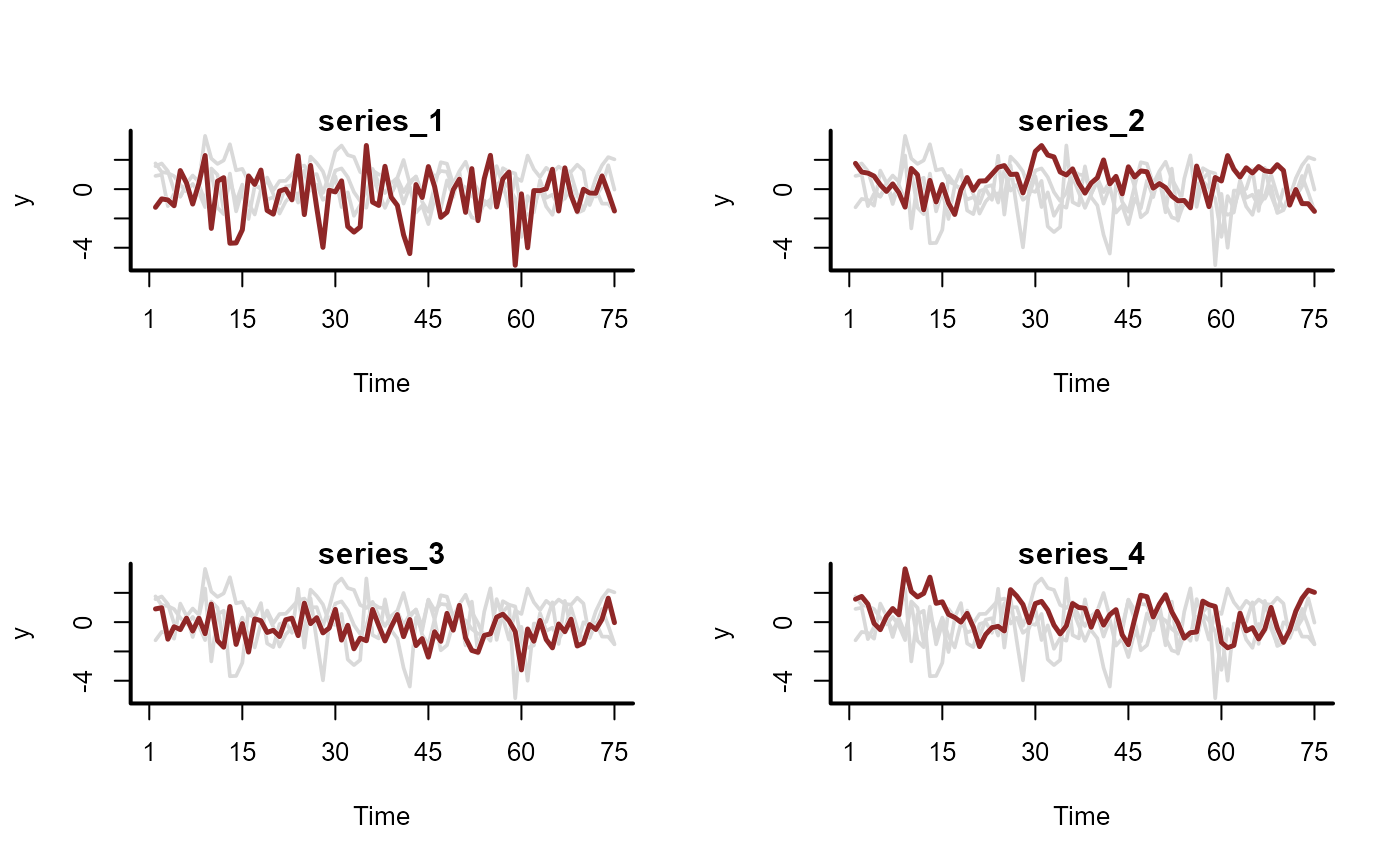

# Fit a model to the portal time series that uses a latent VAR(1)

mod <- mvgam(

formula = captures ~ -1,

trend_formula = ~ trend,

trend_model = VAR(cor = TRUE),

family = poisson(),

data = portal_data,

chains = 2,

silent = 2

)

# Plot the autoregressive coefficient distributions;

# use 'dir = "v"' to arrange the order of facets

# correctly

mcmc_plot(

mod,

variable = 'A',

regex = TRUE,

type = 'hist',

facet_args = list(dir = 'v')

)

#> `stat_bin()` using `bins = 30`. Pick better value `binwidth`.

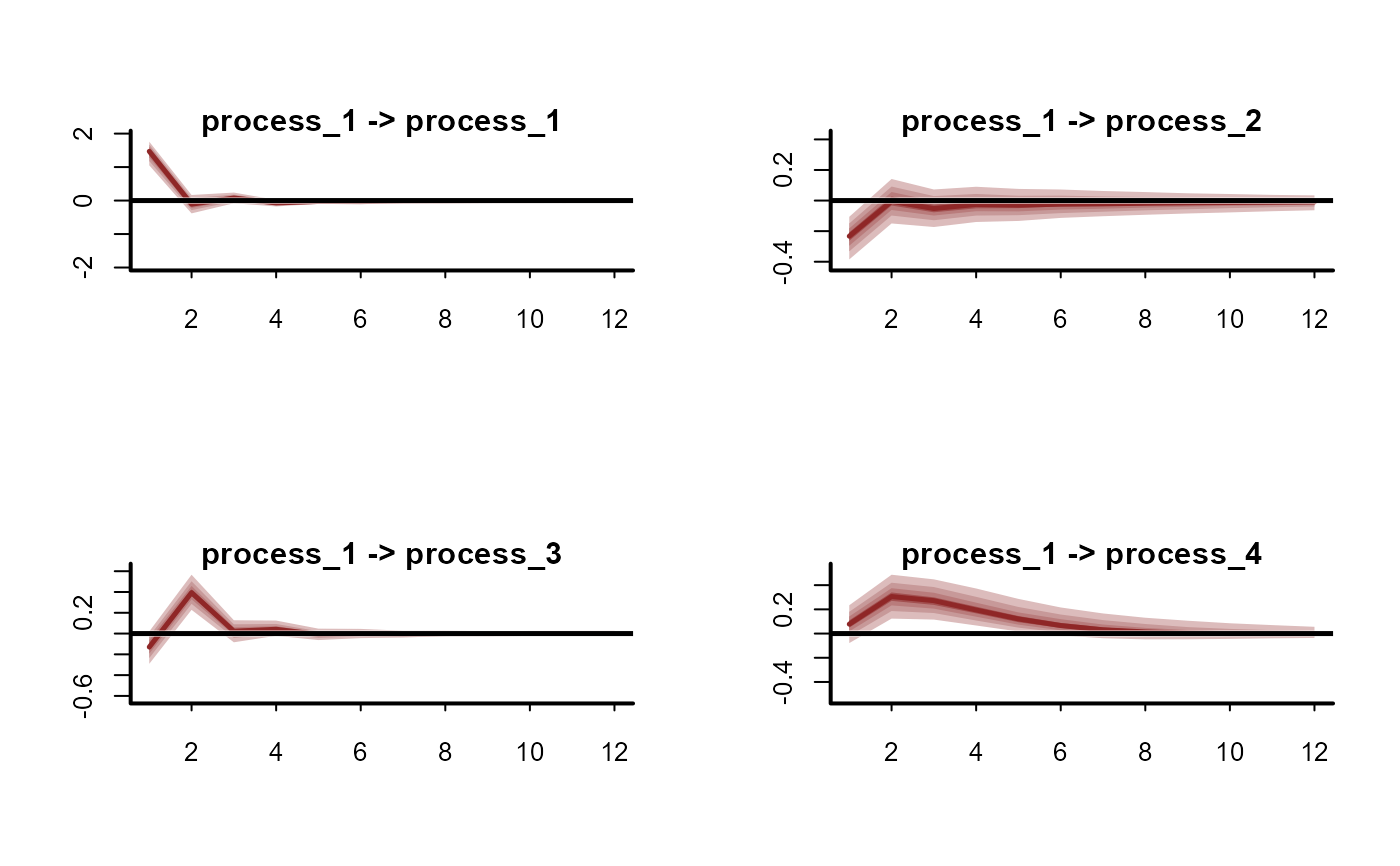

# Calulate Generalized IRFs for each series

irfs <- irf(

mod,

h = 12,

cumulative = FALSE

)

# Plot them

plot(irfs, series = 1)

# Calulate Generalized IRFs for each series

irfs <- irf(

mod,

h = 12,

cumulative = FALSE

)

# Plot them

plot(irfs, series = 1)

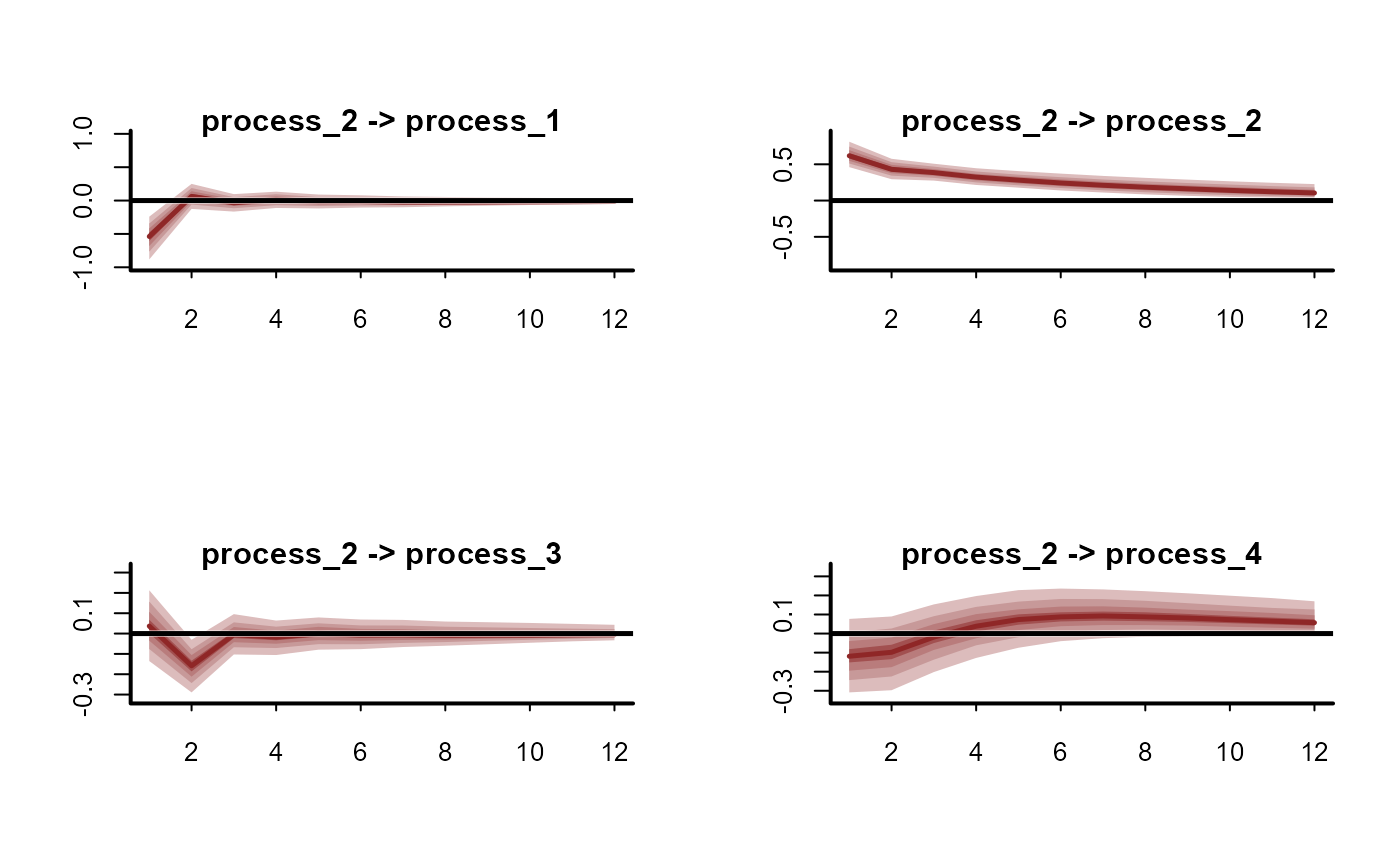

plot(irfs, series = 2)

plot(irfs, series = 2)

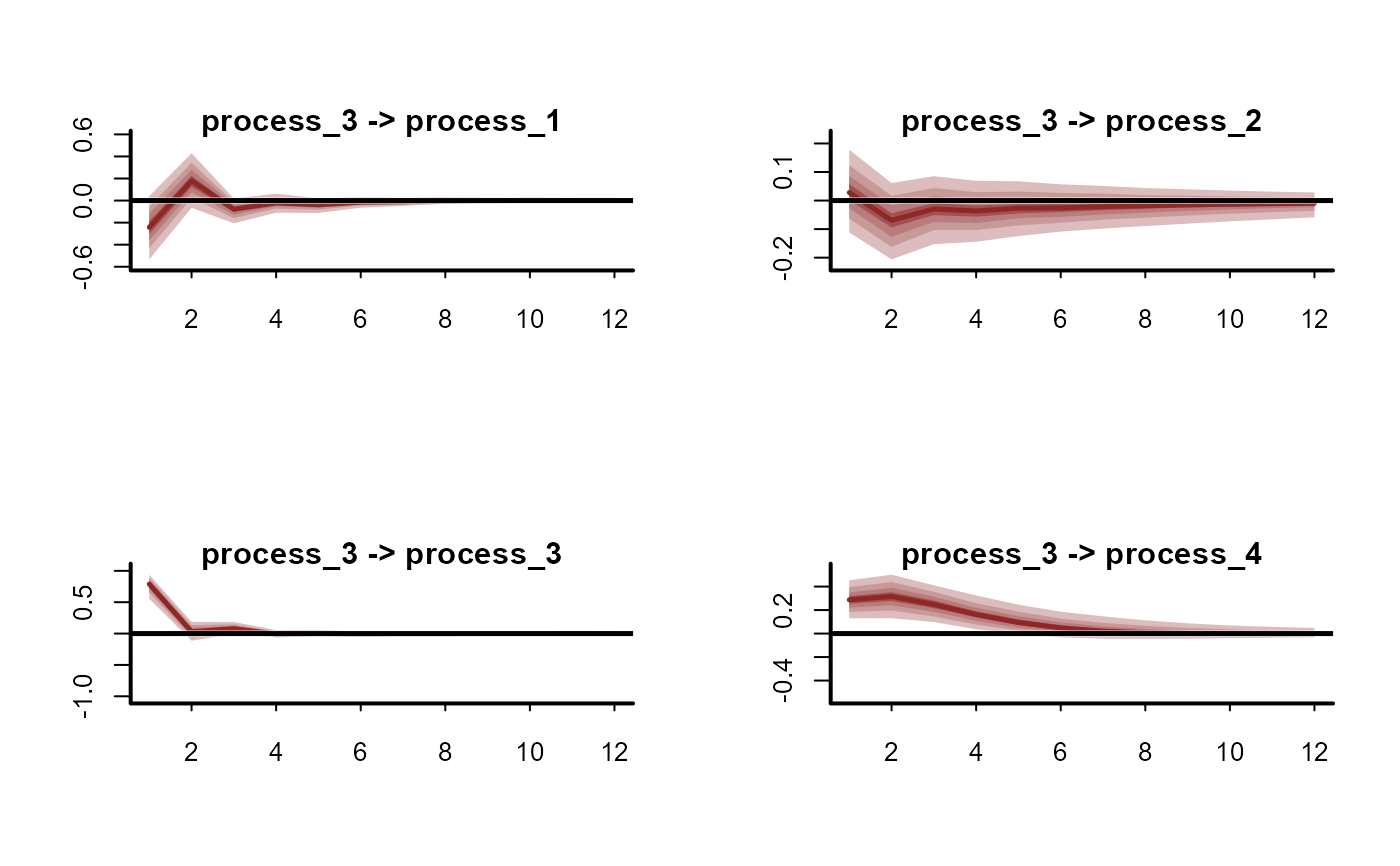

plot(irfs, series = 3)

plot(irfs, series = 3)

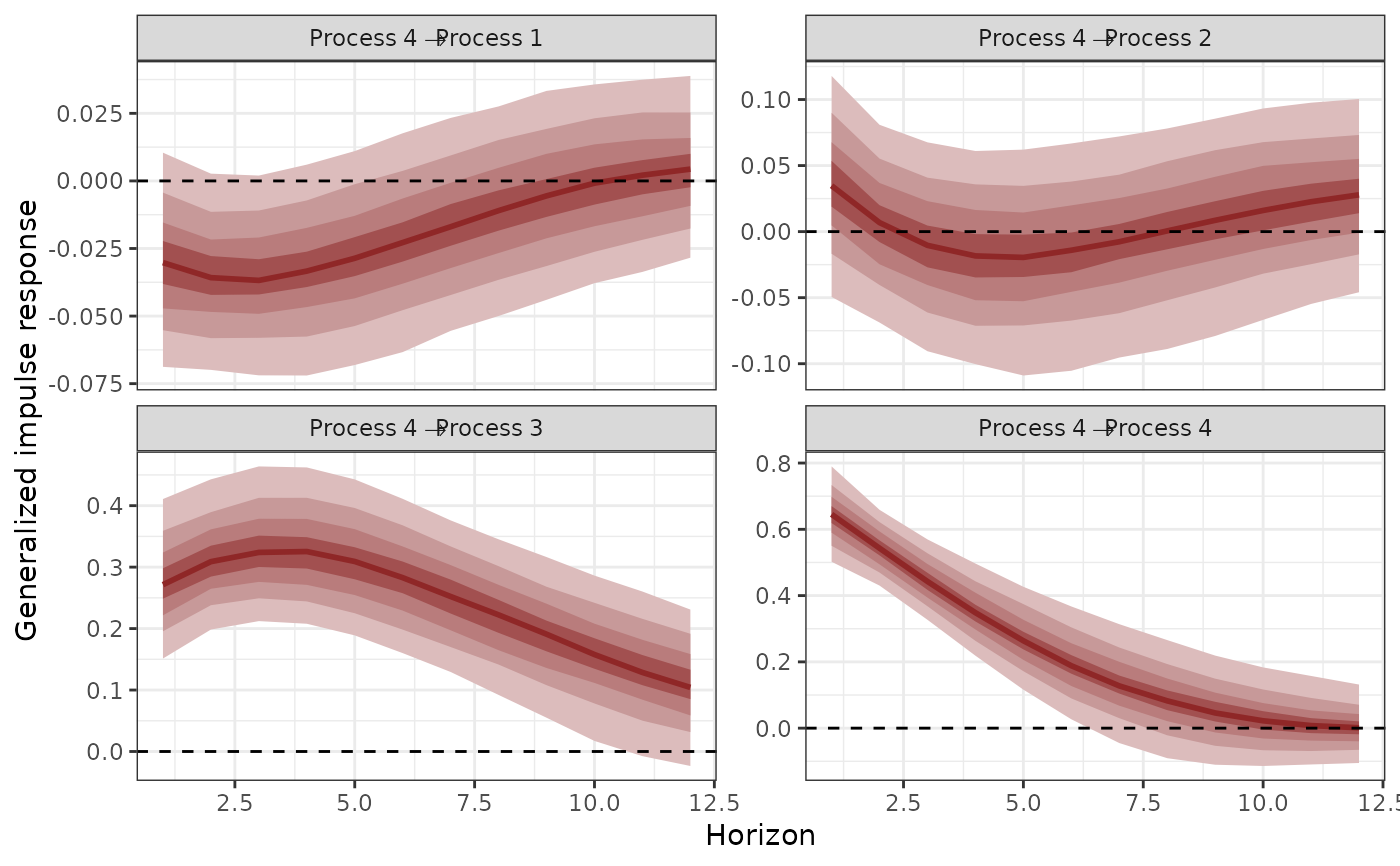

plot(irfs, series = 4)

plot(irfs, series = 4)

# Calculate posterior median, upper and lower 95th quantiles

# of the impulse responses

summary(irfs)

#> # A tibble: 192 × 5

#> shock horizon irfQ50 irfQ2.5 irfQ97.5

#> <chr> <int> <dbl> <dbl> <dbl>

#> 1 Process_1 -> Process_1 1 0.143 0.0886 0.221

#> 2 Process_1 -> Process_1 2 0.131 0.0829 0.197

#> 3 Process_1 -> Process_1 3 0.119 0.0731 0.182

#> 4 Process_1 -> Process_1 4 0.106 0.0624 0.170

#> 5 Process_1 -> Process_1 5 0.0940 0.0486 0.158

#> 6 Process_1 -> Process_1 6 0.0835 0.0370 0.147

#> 7 Process_1 -> Process_1 7 0.0739 0.0258 0.139

#> 8 Process_1 -> Process_1 8 0.0646 0.0160 0.135

#> 9 Process_1 -> Process_1 9 0.0567 0.00877 0.129

#> 10 Process_1 -> Process_1 10 0.0494 0.000988 0.124

#> # ℹ 182 more rows

# }

# Calculate posterior median, upper and lower 95th quantiles

# of the impulse responses

summary(irfs)

#> # A tibble: 192 × 5

#> shock horizon irfQ50 irfQ2.5 irfQ97.5

#> <chr> <int> <dbl> <dbl> <dbl>

#> 1 Process_1 -> Process_1 1 0.143 0.0886 0.221

#> 2 Process_1 -> Process_1 2 0.131 0.0829 0.197

#> 3 Process_1 -> Process_1 3 0.119 0.0731 0.182

#> 4 Process_1 -> Process_1 4 0.106 0.0624 0.170

#> 5 Process_1 -> Process_1 5 0.0940 0.0486 0.158

#> 6 Process_1 -> Process_1 6 0.0835 0.0370 0.147

#> 7 Process_1 -> Process_1 7 0.0739 0.0258 0.139

#> 8 Process_1 -> Process_1 8 0.0646 0.0160 0.135

#> 9 Process_1 -> Process_1 9 0.0567 0.00877 0.129

#> 10 Process_1 -> Process_1 10 0.0494 0.000988 0.124

#> # ℹ 182 more rows

# }